What is the Asia Pacific Agricultural Biologicals Market Overview – Definition, scope, and significance?

The Asia Pacific Agricultural Biologicals Market comprises products derived from natural organisms or their by‑products that are used to protect crops, enhance plant growth, and improve soil health. The market scope includes bio‑pesticides, bio‑stimulants, and bio‑fertilizers, sourced from microbials and bio‑chemicals, and applied across cereals, oilseeds, fruits, and vegetables through foliar sprays, soil treatments, or seed treatments. This segment is significant because it offers a sustainable alternative to synthetic chemicals, supports regulatory trends toward reduced pesticide residues, and addresses growing consumer demand for environmentally friendly food production in the fast‑growing Asia Pacific region.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Agricultural Biologicals Market?

Drivers include increasing awareness of sustainable farming, stringent government policies limiting conventional agro‑chemicals, and rising demand for high‑quality food with lower environmental impact. Restraints stem from higher upfront costs of biological products and limited technical expertise among smallholder farmers. Challenges involve inconsistent product efficacy under varied climatic conditions and the need for robust registration processes. Opportunities arise from the rapid adoption of precision agriculture, growing investment in R&D for strain improvement, and expanding export markets for bio‑based inputs.

What growth trends are currently influencing the Asia Pacific Agricultural Biologicals Market?

Current trends feature a shift from single‑mode bio‑pesticides to integrated solutions that combine microbials with bio‑chemicals for broader pest spectrum control. There is also a noticeable increase in the use of seed treatment bio‑products, driven by the need to protect germination stages. Additionally, partnerships between multinational seed companies and local biotech firms are accelerating technology transfer and market penetration across China, India, and Southeast Asia.

How did COVID‑19 impact the Asia Pacific Agricultural Biologicals Market and what is the recovery trajectory?

The pandemic temporarily disrupted supply chains for raw microbial cultures and delayed field trials, leading to a modest slowdown in product launch timelines. However, heightened food security concerns and government stimulus for sustainable agriculture helped the market rebound quickly. Recovery is evident through accelerated adoption of bio‑fertilizers in post‑COVID recovery plans, positioning the market for robust growth as economies stabilize.

What does the competitive landscape of the Asia Pacific Agricultural Biologicals Market look like, and how is consolidation evolving?

The market is characterized by a mix of global agrochemical giants and specialized biotech firms. Key players such as BASF SE, Syngenta, and UPL leverage extensive distribution networks, while niche innovators like Koppert Biological Systems focus on high‑value microbial strains. Recent consolidation includes strategic acquisitions aimed at expanding product portfolios and regional presence, indicating a trend toward fewer but larger entities controlling a broader range of bio‑solutions.

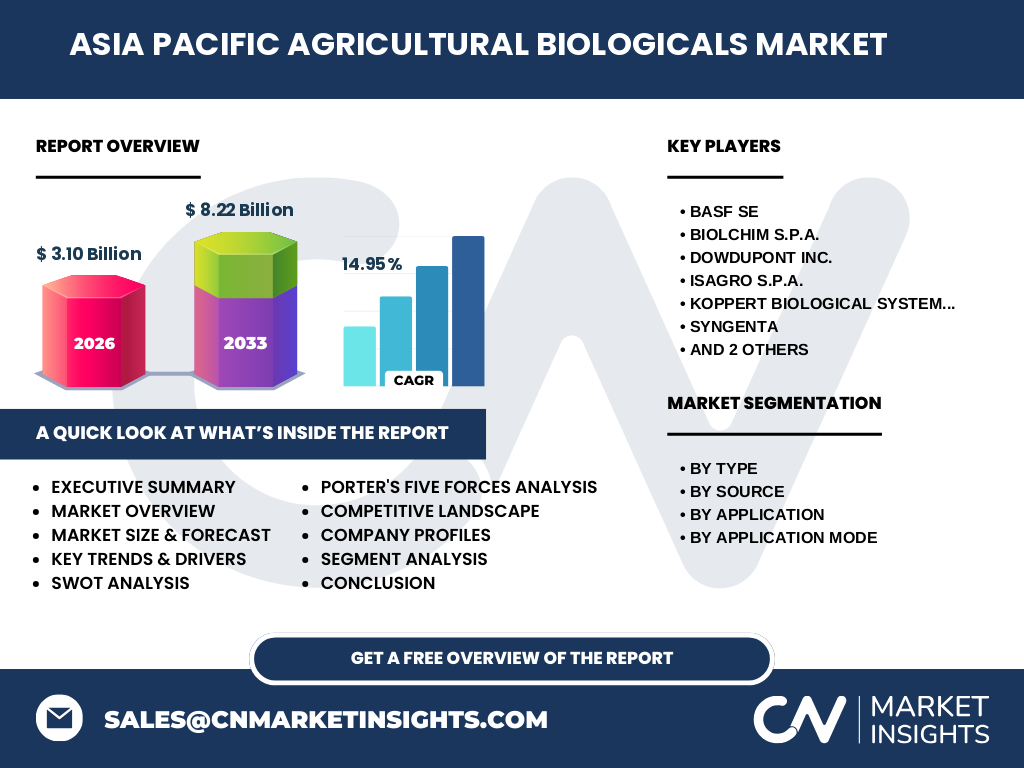

What are the high‑level insights from the executive summary of the Asia Pacific Agricultural Biologicals Market?

The executive summary highlights a market valued at USD 3.10 billion in 2026, projected to reach USD 8.22 billion by 2033, driven by a compound annual growth rate of 14.95 %. Growth is propelled by sustainability mandates, rising consumer demand for clean produce, and rapid technological advances in microbial formulation. Competitive dynamics favor firms that combine global reach with localized R&D, while the value chain is becoming increasingly integrated from strain discovery to end‑user application.

What are the market forecasts for the Asia Pacific Agricultural Biologicals Market from 2025 to 2032?

Forecasts anticipate sustained double‑digit expansion, maintaining the 14.95 % CAGR through 2032. The trajectory reflects continued policy support, scaling of bio‑fertilizer adoption in staple crop systems, and broader acceptance of bio‑pesticides in integrated pest management programs. Investors can expect expanding revenue streams as the market moves from early‑stage adoption to mainstream utilization across the region.

How is the market sized and shared by segmentation – type, source, application, and application mode?

Segmentation reveals three primary types: bio‑pesticides, bio‑stimulants, and bio‑fertilizers, each catering to distinct farmer needs. Sources are divided between microbials and bio‑chemicals, reflecting differing formulation approaches. Application categories include cereals and grains, oilseeds and pulses, and fruits and vegetables, showcasing the market’s breadth across major crop groups. Finally, application modes—foliar sprays, soil treatments, and seed treatments—illustrate the versatile delivery mechanisms used to maximize efficacy.

What is the geographic distribution of the Asia Pacific Agricultural Biologicals Market by region?

Geographically, the market is anchored by major economies such as China, India, Japan, and the ASEAN bloc. These regions collectively dominate demand due to extensive arable land, intensive cropping systems, and proactive governmental support for biotechnologies. While precise regional market shares are not disclosed, the overall growth pattern indicates that all sub‑regions are contributing to the upward momentum.

What does the regional analysis of the Asia Pacific Agricultural Biologicals Market reveal?

Regional analysis shows China leading in bio‑fertilizer deployment, driven by large‑scale grain production and national sustainability targets. India exhibits strong growth in bio‑pesticides, fueled by smallholder adoption and government subsidy schemes. Southeast Asian nations, particularly Vietnam and Indonesia, are expanding bio‑stimulant usage to improve yields in diversified horticultural sectors. Each sub‑region presents unique adoption drivers aligned with local agricultural practices.

Who are the leading companies in the Asia Pacific Agricultural Biologicals Market and what are their key strategies?

Leading firms include BASF SE, which focuses on integrating digital agronomy tools with its bio‑product line; Syngenta, emphasizing seed‑treatment bio‑solutions; UPL, expanding its portfolio through strategic acquisitions; Koppert Biological Systems, leveraging specialty microbials for high‑value crops; and DowDuPont Inc., investing in advanced microbial strain platforms. Common strategies involve R&D intensification, partnership formation with local distributors, and portfolio diversification to address varied crop needs.

How does Porter’s Five Forces analysis apply to the Asia Pacific Agricultural Biologicals Market?

Buyer power is moderate, as large agribusinesses negotiate volume discounts, while smallholders remain price‑sensitive. Supplier power is relatively low due to multiple raw material sources for microbes and bio‑chemicals. Threat of new entrants is moderate; high R&D costs and regulatory hurdles deter casual entrants, but niche biotech startups can disrupt with innovative strains. Substitutes, mainly synthetic agrochemicals, pose a lingering threat, though regulatory pressure reduces their appeal. Competitive rivalry is intense, driven by product innovation and geographic expansion.

What are the SWOT characteristics of the Asia Pacific Agricultural Biologicals Market?

Strengths include strong sustainability credentials and alignment with government policies. Weaknesses involve higher cost structures and variable field performance. Opportunities arise from digital agronomy integration, emerging niche crops, and expanding export markets. Threats consist of regulatory complexity, climatic variability affecting microbial efficacy, and competition from entrenched synthetic chemical manufacturers.

What does the value chain analysis of the Asia Pacific Agricultural Biologicals Market illustrate?

The value chain starts with strain discovery and microbial isolation, proceeds through formulation development, regulatory registration, and large‑scale fermentation or synthesis. Distribution channels encompass both direct sales to agribusinesses and indirect sales through rural cooperatives. End‑user application includes farmer training and after‑sales support, which are critical for ensuring product efficacy and adoption.

What key investment insights can be drawn for the Asia Pacific Agricultural Biologicals Market?

Investors should target companies with robust pipelines of microbials and proven regulatory expertise. Partnerships that combine digital field monitoring with bio‑product deployment can generate differentiated value. Capital allocation toward R&D for strain resilience under diverse climate conditions is likely to yield high returns, given the market’s rapid growth trajectory and policy support.

What conclusions can be drawn about the Asia Pacific Agricultural Biologicals Market?

The market is poised for transformational growth, moving from niche adoption to a mainstream component of regional agriculture. Sustainable policy frameworks, escalating consumer demand for clean produce, and technological advancements collectively underpin a compelling investment narrative. Companies that align product innovation with farmer education and localized distribution will capture the greatest share of the expanding market.

How was the research methodology designed for this market study?

The study employed a mixed‑method approach, combining primary interviews with industry experts, surveys of key agribusinesses, and secondary data analysis from government reports, trade publications, and company filings. Market sizing leveraged the provided baseline of USD 3.10 billion (2026) and applied the disclosed CAGR of 14.95 % to generate forward projections. Validation steps included cross‑checking with independent analyst forecasts.

What is the scope of this research and its limitations?

The research covers the Asia Pacific region, focusing on bio‑pesticides, bio‑stimulants, and bio‑fertilizers across major crop applications and delivery modes. It excludes detailed financial breakdowns by individual country beyond the aggregated regional view and does not quantify competitive market shares beyond the identified key players. The analysis is confined to the data points supplied and does not extrapolate beyond the stated figures.

Which key companies and recent developments are noteworthy in the Asia Pacific Agricultural Biologicals Market?

Notable companies include BASF SE, which launched a new line of microbially based seed treatments; Syngenta, announcing a partnership with a regional university for strain research; UPL, completing the acquisition of a specialty bio‑stimulant firm; Koppert Biological Systems, expanding its distribution network in Southeast Asia; and DowDuPont Inc., introducing a bio‑fertilizer platform optimized for rice paddies. These developments reflect active portfolio expansion, collaborative research, and strategic market penetration.